Tech companies are always seeking new customers, and Cash App, owned by Jack Dorsey’s Block, sees potential in targeting children. The company, which already provides services to teens, is expanding its youth-focused offerings to connect with Gen Alpha and upcoming adolescents in the U.S.

The new initiative allows parents to create financial accounts for children aged 6 to 12. These accounts are managed by parents, who can deposit and monitor funds, while children receive a debit card linked to these accounts for spending.

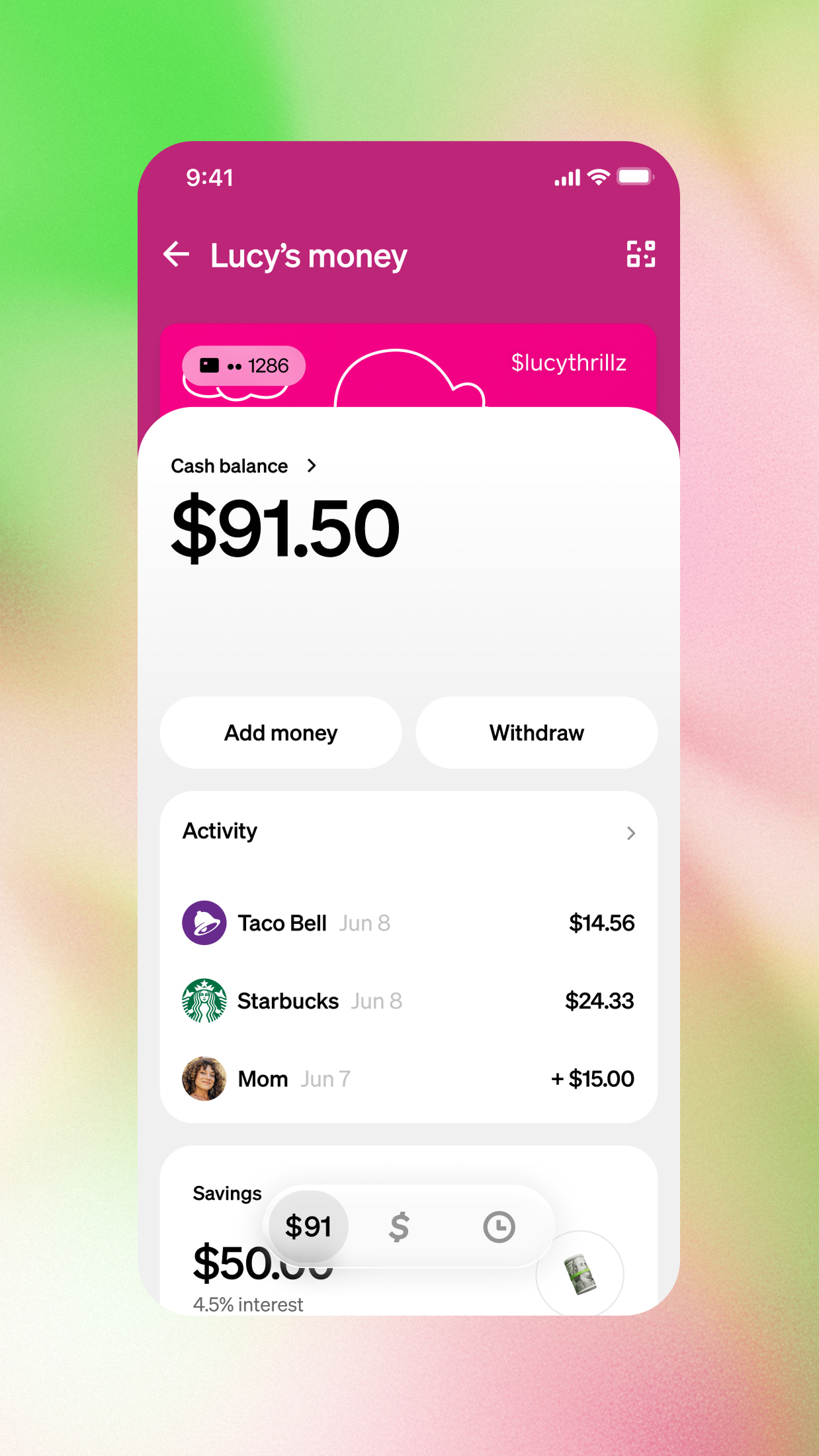

The accounts can accept P2P payments from approved users (like grandparents) and earn up to 3.25% interest. This effort aims to teach children about financial responsibility, according to Kristen Anderson, Cash App’s group product lead for Core Networks. Anderson highlighted the desire to engage kids earlier in financial learning, aided by the app’s “allowance” feature for automated transfers.

Once children turn 13, they can transition to their own Cash App accounts with parental consent. At 13, they gain access to more services, including buying/selling bitcoin and trading stocks, which require adult oversight until they’re 18.

Cash App reports having 5 million monthly active teen users, according to Owen Jennings, executive officer and head of business at Block.

Other platforms also offer fintech services to children. MrBeast, the viral TikTok star, recently faced scrutiny over acquiring Step, which serves users under 18. Some advocate these services for teaching financial literacy, while critics argue they may achieve the opposite.